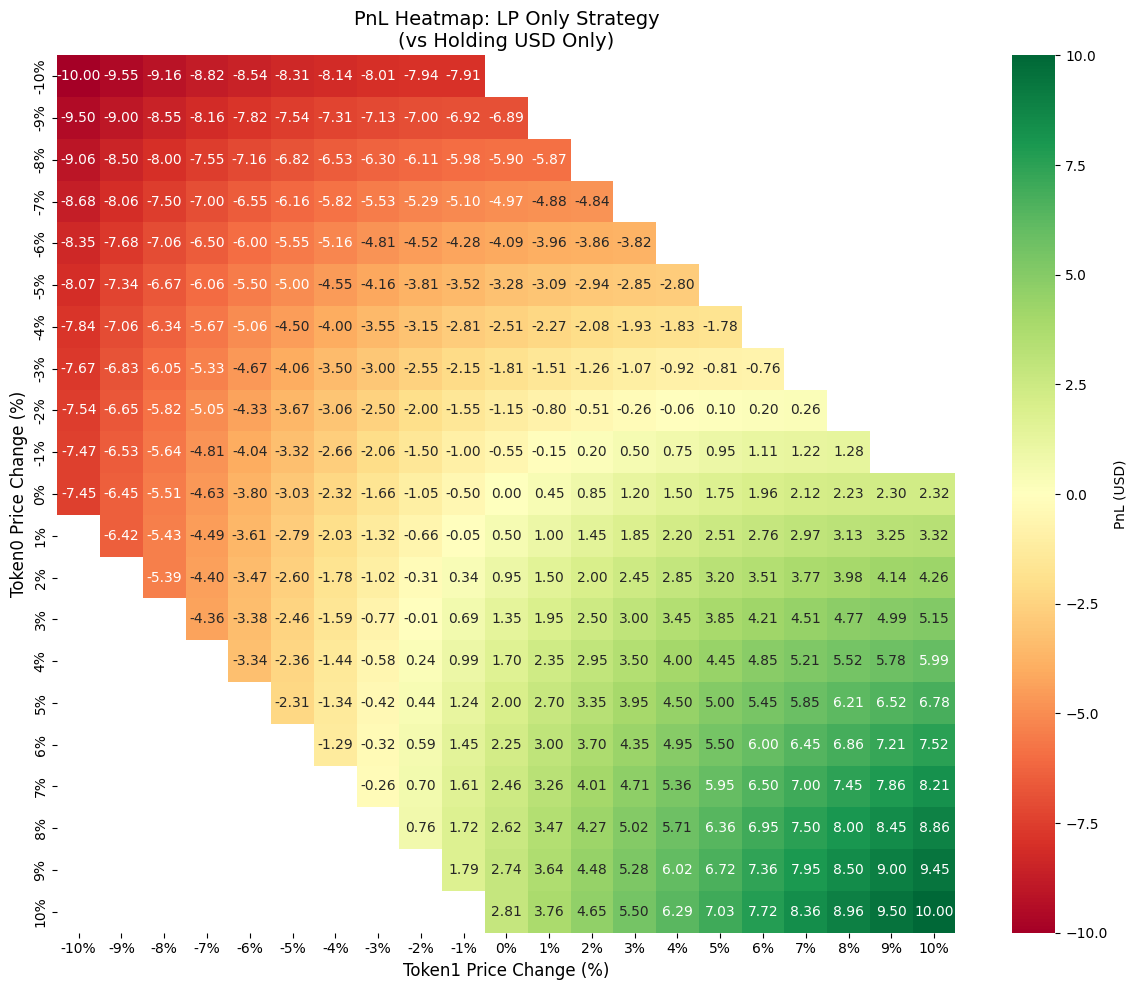

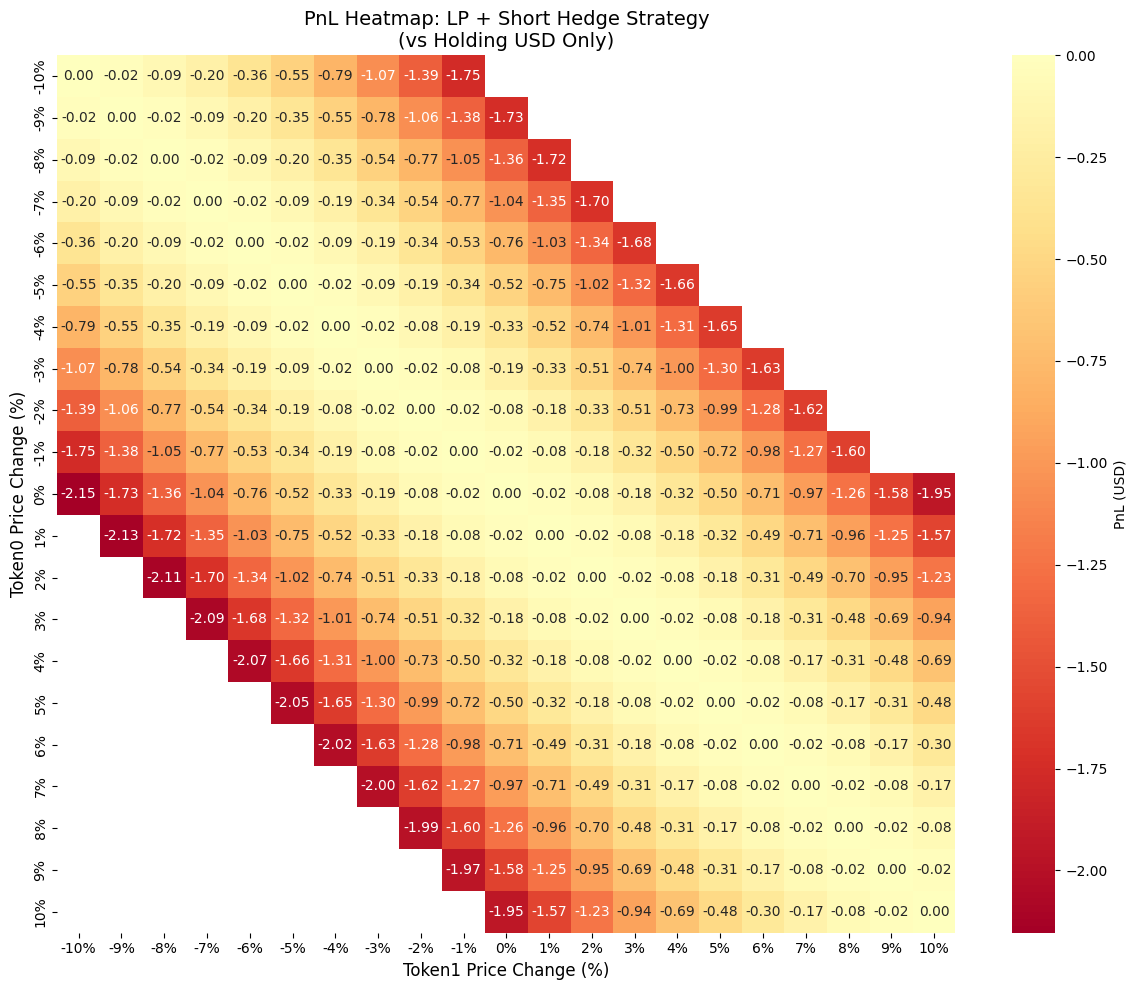

To understand Huam’s hedging approach, let’s walk through a concrete example. Assume we enter an ETH-USDC pool on Uniswap V3 with a symmetric ±10% price range centered on the current price. Our initial deposit is 1 ETH and 3,000 USDC (assuming ETH price is $3,000). This LP position earns trading fees from swaps that occur within our range. However, it is also exposed to impermanent loss (IL)—the difference in value between holding the LP position versus simply holding the original assets. As price moves away from the entry point in either direction, IL increases.