Selecting Option Maturity

However, introducing options requires us to specify a maturity date, which brings us to the next consideration. To determine the appropriate option tenor, we estimate how long the LP position is expected to remain in range. If price exits the range, the LP position stops earning fees and must be closed or repositioned. Assuming the underlying asset follows a driftless geometric Brownian motion (GBM), we can derive the expected time to reach a given price boundary. For a return level (the distance to the range boundary as a percentage), the expected time is: where is annualized volatility. Example: ETH volatility = 60%, price range = ±20% This calculation guides our option maturity selection: we match the option tenor to the expected duration of the LP position. Tighter ranges mean shorter expected durations and therefore shorter-dated options.Evaluating Profitability

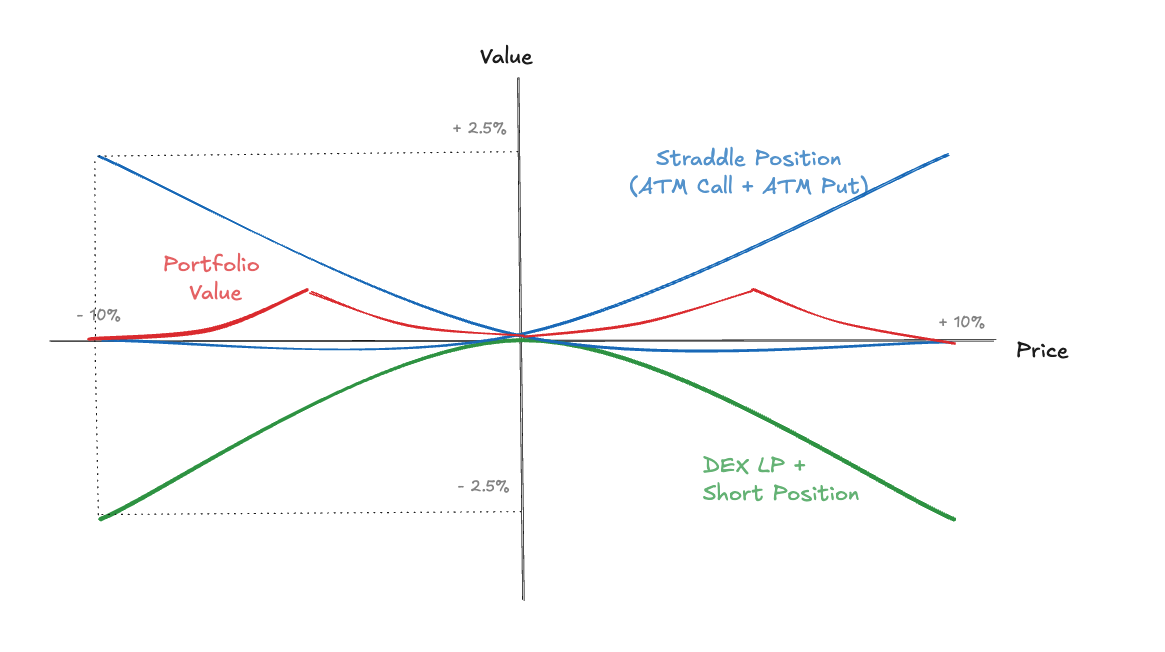

With the hedging framework established, the profitability condition becomes straightforward: If the fees earned from the LP position plus any funding payments received from the short perpetual exceed the cost of the options hedge, the position is profitable. It’s important to note that adding options does not magically create yield where none exists. If a pool’s fee revenue is fundamentally insufficient relative to the volatility of its underlying assets, the hedge simply reshapes the risk profile without improving the economics. The option premium reflects the expected cost of the volatility exposure we’re hedging away. However, this framework provides two significant benefits:- Variance reduction: By hedging IL, we dramatically reduce the volatility of returns. The position generates more consistent yield across different price paths, rather than being highly profitable in some scenarios and deeply unprofitable in others.

- Rigorous evaluation: Using established option pricing models allows us to evaluate opportunities on a sound theoretical basis. Rather than naively selecting pools with the highest displayed APY, we can compare fee revenue against the true cost of the associated risks.