- Borrow & Deposit: You deposit stablecoins (e.g., USDC) into a lending protocol, borrow the volatile asset (e.g., ETH), and pair them to provide liquidity.

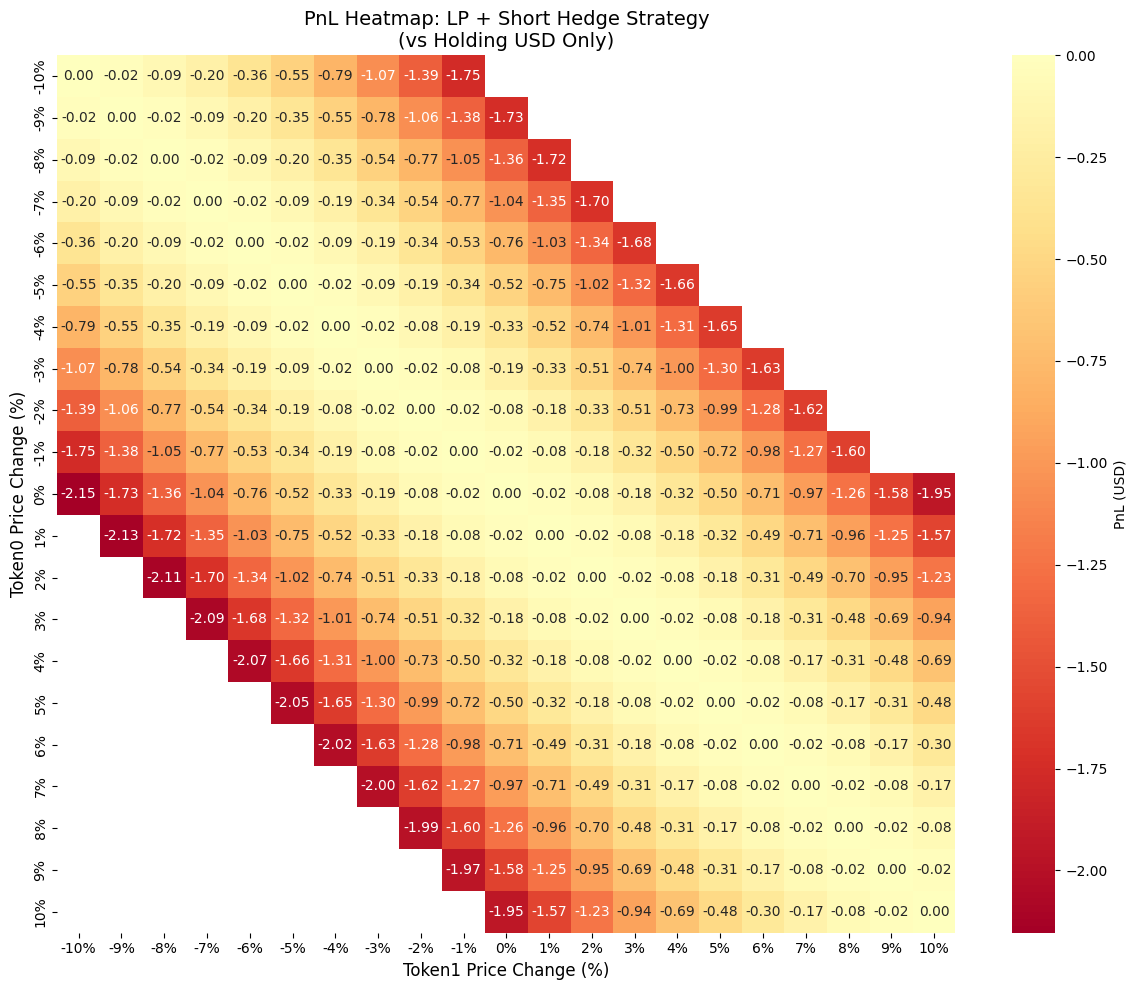

- Deposit & Hedge: You provide liquidity using your own capital (ETH + USDC) and simultaneously open a short position of equal value on a perpetual exchange.

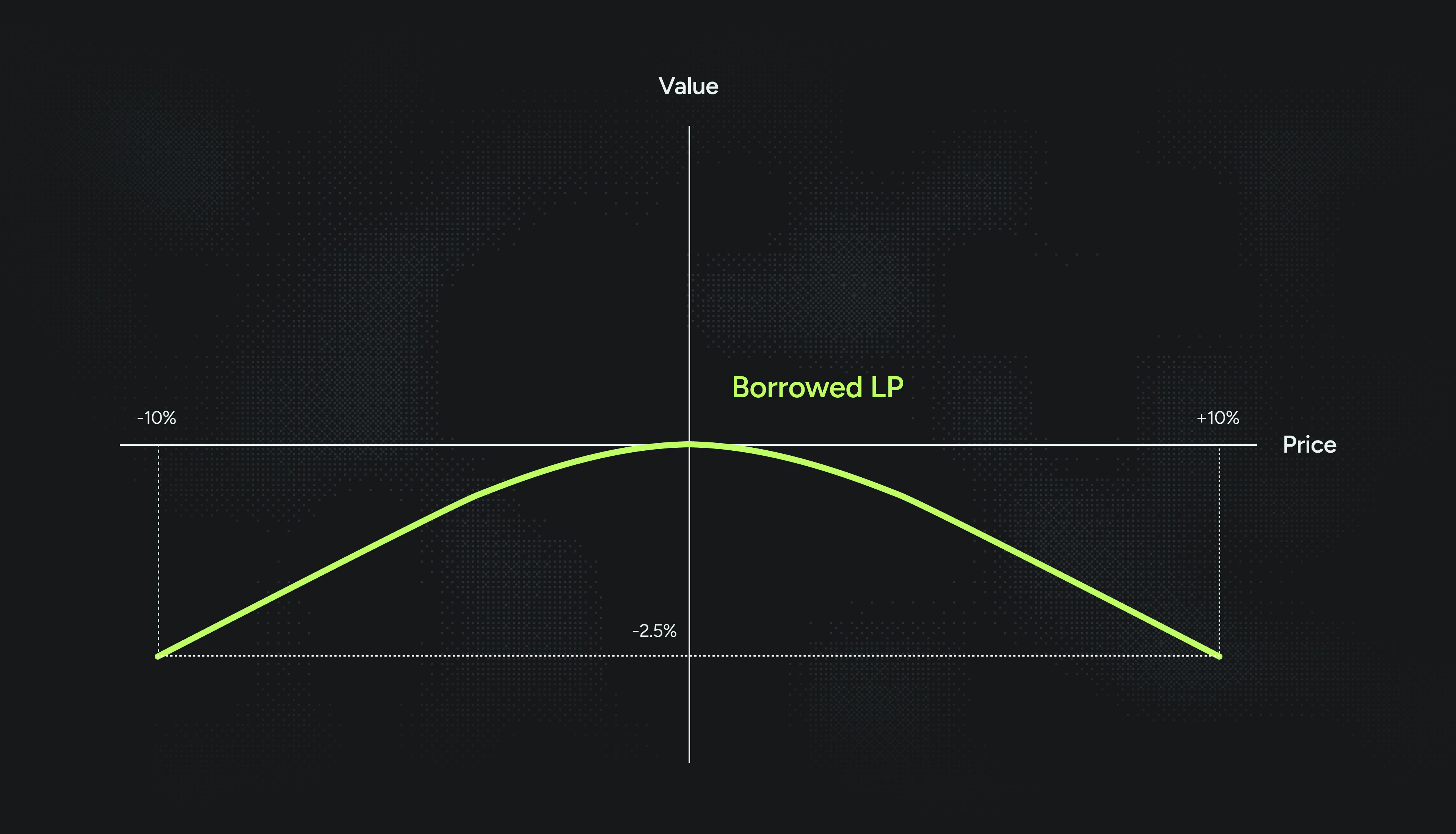

Concave PnL Profile

The key structural feature is that the LP position is short gamma. While the hedge (short perp or debt) introduces a linear payoff, the AMM inventory rebalancing produces a concave payoff profile. Subtracting a linear hedge from a concave curve preserves the concavity, resulting in negative convexity overall. Ignoring fee income, the position’s mark-to-market value is maximized at the entry price . As price moves away from this level in either direction, the position loses value.

- The Short Hedge (or debt) is linear. If price moves +10%, the short loses exactly 10%.

- The LP Position is non-linear (concave). As price rises, the LP sells the appreciating asset (ETH) for the stable asset (USDC). It captures less upside than a simple hold.

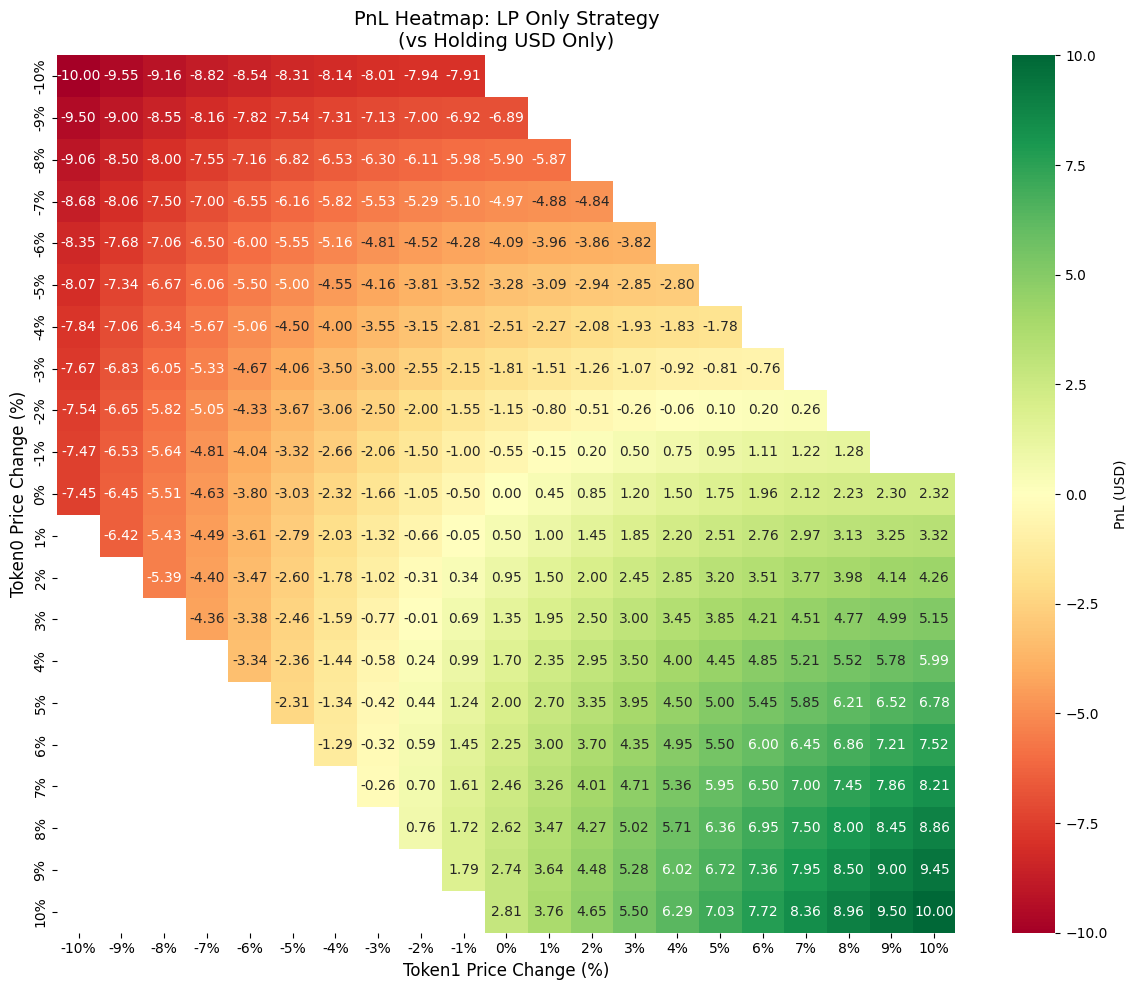

Why the LP Position Bleeds on Volatility