- Static hedge: A short perpetual removes directional exposure, making the position delta-neutral at inception.

- Dynamic hedge: Continuous rebalancing of the perpetual position replicates a long straddle, offsetting the concave loss profile of impermanent loss.

Static Hedge: Removing Delta

Before addressing the curved loss profile, we first remove directional exposure. At the moment of entering an LP position, the protocol holds some amount of the volatile asset (e.g., ETH). If price rises 10%, that ETH holding gains 10%—this is unwanted directional exposure. To neutralize this, the protocol opens a short perpetual position sized to match the ETH balance in the LP. If the LP holds 10 ETH, the protocol shorts 10 ETH worth of perpetuals. This static hedge removes the “first-order” price sensitivity. But it does nothing about the curved loss profile—the impermanent loss that accumulates as price drifts away from entry. That requires a different approach.Dynamic Hedge: Manufacturing Convexity

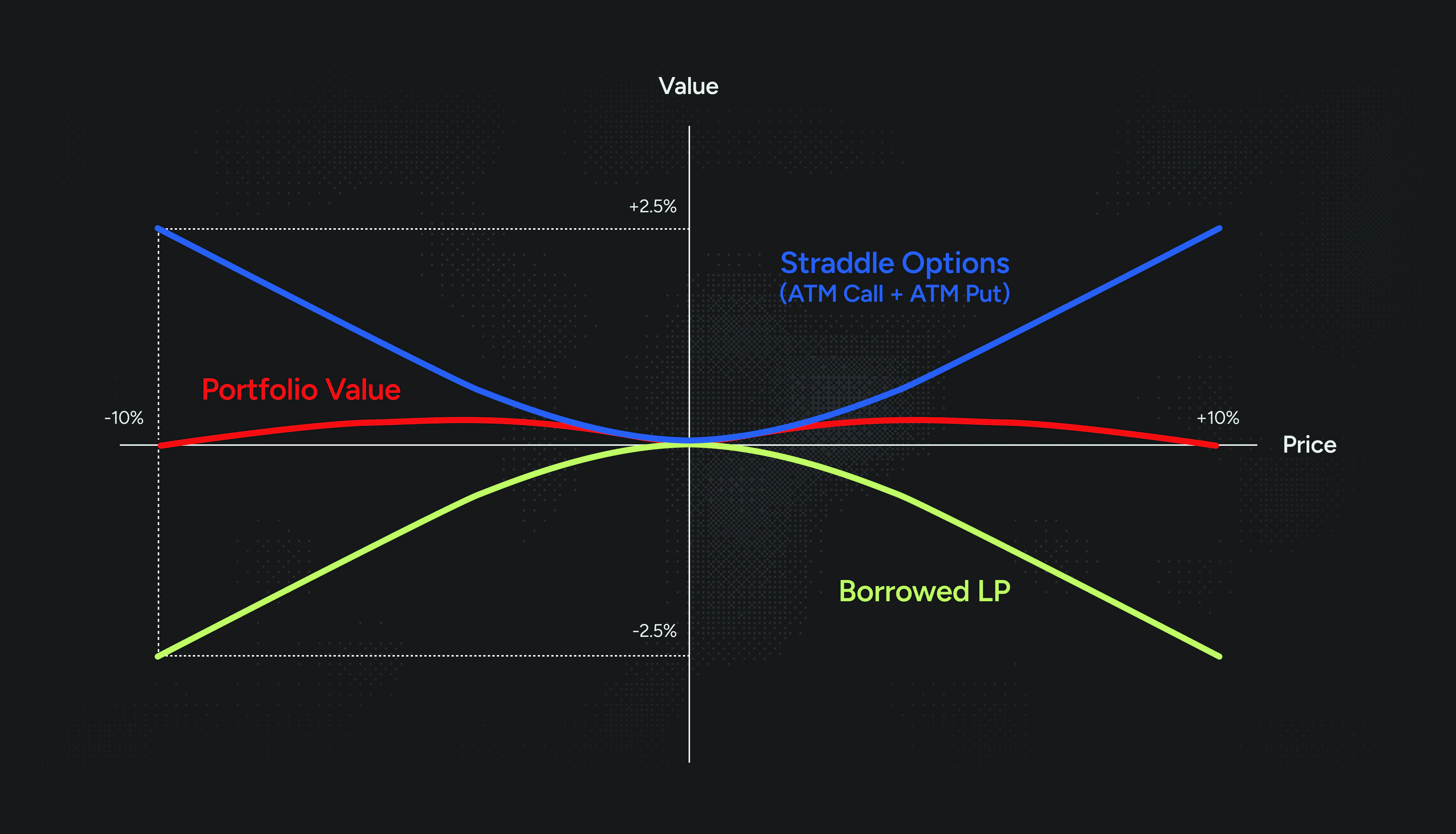

If the LP behaves like a short straddle, the natural hedge is a long straddle—a position that gains value when price moves in either direction. Combining these two should produce a flat PnL profile: the LP’s losses are offset by the hedge’s gains. The challenge is that we can’t simply buy a straddle. Crypto options markets are thin, expensive, and only exist for major assets like BTC and ETH. For the vast majority of token pairs—ARB/USDC, CRV/WETH, and countless others—there is no options market at all. Instead of buying an option, we can replicate the payoff by continuously trading the underlying asset. Any option payoff can be replicated by continuously trading the underlying asset. A straddle gains value when price moves because its “delta”—sensitivity to price—changes as price moves. At the entry price, a straddle has near-zero delta. As price rises, the call becomes more valuable and the straddle becomes increasingly long. As price falls, the put dominates and the straddle becomes increasingly short.| Price Movement | What Happens to LP | Required Hedge Adjustment |

|---|---|---|

| Price rises | LP sells ETH into the rally (becomes “shorter”) | Buy back some of the short perpetual |

| Price falls | LP accumulates ETH on the way down (becomes “longer”) | Increase the short perpetual position |

Cost of the Synthetic Hedge

Dynamic replication isn’t free. Each rebalancing trade incurs costs:- Realized Loss due to rebalancing portfolio to track the delta of the straddle

- Transaction costs on the perpetual exchange

- Funding payments (which can be positive or negative depending on market conditions)